- Revenue increased by 3.3% while gross profit increased by 18.6% as product buy up activities ahead of price increases effective mid-March and mid-April 2019.

- Distribution and selling and admin expenses remain flat which is good.

- Profit before tax increased by 83% due to higher sales and lower import cost primarily attributed to favorable foreign exchange impact.

- Operating cash flow generated from operating were RM 51 million for 6 month cumulative which accounts for full year operating cash flow for the past 3 years.

- The company has a net cash of RM 198 million which equivalent to RM 1.21 net cash per share.

- Movement of USD/MYR for April, May & June 2019. Its average is around 4.15.

- The management is optimistic of Amway growth in 2019.

Comments

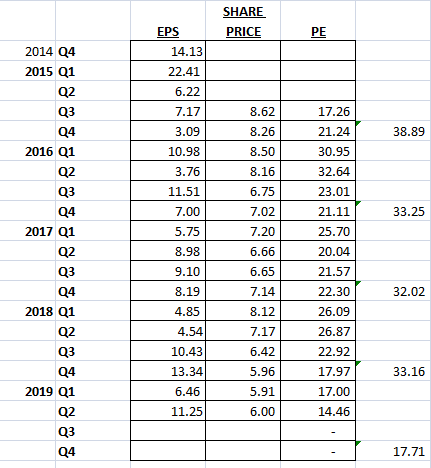

- The net profit margin improved to 6.1% which is the highest level since 2016 as Amway increase their product price effective April 2019. This is something worth taking note as dividend payout ratio of Amway is 80% - 90%. Therefore, increase in EPS would lead to increase in dividend payout.

- Assuming if the EPS for the year is 35 sen, 85% dividend payout would be 30 sen. At RM6 a share, its DY is 5%.

- At RM6 a share, its PE is 14.4 which is the lowest in 5 years. As mention in my previous post, a reasonable PE for Amway is 18 - 20. Assuming Amway is able to achieve an EPS of 35 sen, At PE 18 Amway is worth RM6.30. At PE 20, Amway is worth RM7.

No comments:

Post a Comment