- 37.84% of its shares is owned by its parent company in taiwan YSP International Company Limited which is a subsidiary of Yungshin Global Holdings Corp listed in Taiwan. Top 30 shareholders accounts for 76% of its shares.

- YSPSAH is Yungshin Global's investment arm in South East Asia. From the above info, we can see that YSPSAH gross profit margin, PBT margin, ROE are quite identical to its mother company.

- Export licences held by YSPSAH totalled 1,232 and they consisted of pharmaceutical, veterinary and aquatic, cosmetic, and Traditional Chinese Medicine (TCM) products as well as medical devices.

- The total registered products for Y.S.P.SAH ballooned to 464 (420 in the previous year) and they are made up of 355 pharmaceutical products and 109 veterinary products (approximately 25% of its products are veterinary products)

- YSPSAH has 3 manufacturing plants:-

- Malaysia - manufacturing plan in Bangi has recently just upgraded to reduce cost and increase efficiency by adding machinery to boost the production capacity. New tablet press machines, new high-speed packing machines, and packaging material automatic counting and folding machines to optimize processes.

- Vietnam - pharmaceutical and veterinary factory in Vietnam, has added a new production line – Beta-lactam production line. This was completed and granted GMP status in mid-2018. 89 new products were registered in Vietnam in the year under review.

- Indonesia - PT. YSP Industries Indonesia (PTYSPII) pharmaceutical plant embark on adding a new Solid Line in the new financial year in the effort to increase its product line to include tablets and capsules.

- Most of YSPSAH products are sold to private clinics, hospitals and pharmacies which accounts for 75%, 15% of income are from veterinary and aquatic products while OTC products accounted for 10%.

- 95% of YSPSAH revenue and PBT were contributed from manufacturing of pharmaceutical products and its profit margin is ranged from 11% - 14%.

- Worth to acknowledge that the directors salary is only 3.8% of its profit before tax.

- 72.7% of its sales were derived in Malaysia with the remaining 27.3% from exports.

- Sales in export markets increased 4.9% while local market increased 12.5% in 2018 from 2017.

- It is also worth taking note that it doesn't have any single client that contributes more than 10% of its revenue which is a big plus plus for YSPSAH.

Pharmaceutical Industry

- The domestic pharmaceutical market as a whole valued at RM7.5 billion as at the third quarter of 2018 by the Malaysian Pharmaceutical Association of Malaysia.

- Generic drugs accounts for 21% (copies of brand-name drugs that have exactly the same dosage and effects as the original drug) , over-the-counter (OTC) medicines 24% (medicines sold directly to a consumer without a prescription from a doctor) and originator drugs 55% (the first drug containing its specific active ingredients to receive approval for use)

- Market growth has been relatively fast, at between 8 and 10 per cent annually in the last decade.

- Local pharmaceutical manufacturing companies only account for less than 30% of Malaysia's drugs market share with remaining 70% being imported drugs.

- According to the Malaysian Organization of Pharmaceutical Industries (MOPI), Malaysia manufacturers currently export to countries in Southeast Asia, Africa and the Middle East. Growth in exports has been climbing steadily at 10-12% annually

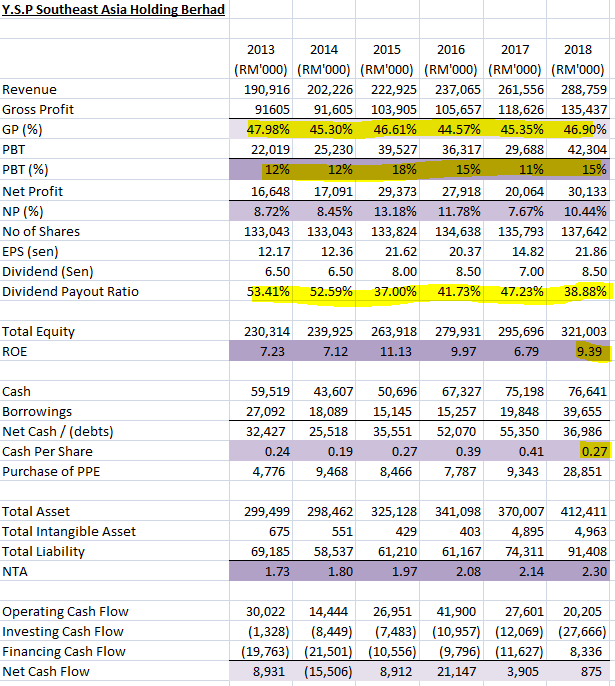

Financial Highlight

- Revenue grew at CAGR of 7% from 2013 - 2018.

- Gross profit margin were steady over the 6 years between 45% - 50%.

- PBT margin were steady over the 6 years which is above 10%.

- Dividend payout ratio range between 30% to 50%.

- ROE is decent at 10%.

- The borrowings increased by 100% in 2018 as compared to 2017 is due to its purchase of PPE of RM 28 million.

- Net cash company with RM 0.27 sen of cash per share in 2018.

- YSPSAH spend RM 28 million on purchase of plant & equipment which is the highest since 2013. (however, will that translate into higher efficiency in the coming 2 years?)

- The total profit before tax for YSPSAH is RM 195 million over the 6 year where the operating cash flow generates were RM 161 million (meaning they manage to turn all their sales into cash)

Futures Prospect

- Expansion of the plant in Bangi, Selangor, which will result in the oral solid dosage manufacturing capacity being doubled. The utilisation capacity has reached 70 per cent in current round-the-clock operation.

- Increase the storage capacity of the raw material warehouse as well as the introduction of “online” pre-packing to reduce manual human operation resulting in greater cost savings.

- Venture into technological advanced manufacturing process will be in collaboration with local institution.

- Further expansion of product portfolio from pharmaceutical to veterinary, Over-the-Counter, medical devices and food supplements.

- In the area of exports, the plan is to increase participation in Government tenders in ASEAN and African countries and also to advance into developed and regulated markets such as Canada, Australia, and New Zealand.

Strength

- Being a subsidiary of Yungshin Global Holding Corp give them access to its parent's company technology and expertise.

- Enjoy the global trademark or brandname of Y.S.P as Y.S.P currently has presence in South East Asia, Japan, US, China and Taiwan.

- Overseas market only accounts for 30% of YSPSAH revenue, therefore, there are more room for them to grow. (However the donwside to this is that most of South East Asia countries like Myanmar, Vietnam, Cambodia and Indonesia has low awareness on heathcare)

- Low single customer risk (YSPSAH do not have any single customer that contributes more than 10% of its revenue).

- Solid balance sheet and consistently generate positive cash flow through its operating.

- Stable earnings ability (YSPSAH did not have any loss making quarter since 2007)

- Demand for drugs and medicines are always on the rise and is less cyclical.

Weakness

- YSPSAH products are mostly generic drugs therefore, YSPSAH has not much competitive advantage over other pharmaceutical companies in term of products differentiation.

- Most of YSPSAH clients are private hospital, clinics and pharmacies and is lacking of government hospital contracts which consume more generic drugs as they are cheaper compare to patterned drug.(this is also their strength as they do not need to depends on government to do business)

- YSPSAH needs to compete with foreign pharmaceutical companies in Malaysia market, as import of drugs are tariff free as it is medical supplies.

- Lack of institutional/fundhouse holding it (there is only one fund which is PB ISLAMIC SMALLCAP FUND appear as its top 30 shareholders)

Peer to Peer Comparison

- Dpharma (Market Cap: RM 880 M, PE: 18.42, ROE: 9.89, DY: 6.40%, Profit Margin: 9.6%, Gearing ratio: 30%)

- Ahealth (Market Cap: RM 1.03 B, PE: 17.69, ROE: 15.30, DY: 1.53%, Profit Margin: 9%, Net cash: 0.43/share)

- Kotra (Market Cap: RM 247 M, PE: 12.54, ROE: 11.93, DY: 2.91%, Profit Margin: 11.4%, Gearing ratio: 14.3%)

- Pharma (Market Cap: RM 630 M, PE: 14.85, ROE: 8.32, DY: 6.61%, Profit Margin: 1.8%, Gearing ratio: 115%)

- Yspsah (Market Cap: RM 330 M, PE: 10.90, ROE: 9.57, DY: 3.57%, Profit Margin: 10.5%, Net cash: 0.27/share)

* Out of the 5 companies, only YSPSAH and Ahealth are net cash company and YSPSAH has the lowest PE.

Valuation @ RM2.38

- At current price of RM 2.38, YSPSAH is trading at PE of 10.90 and its dividend yield is 3.5%.

- At PE of 10 its share price will be RM 2.18 and DY will be 3.9% (so anything below this, i will say there is a margin of safety).

- From above peers comparison, the fair PE for pharmaceutical company range between 12 - 15. At PE 12, YSPSAH is worth RM 2.62. At PE 15, YSPSAH is worth RM 3.25 (this is based on the assumption that YSPSAH is able to at least maintain its earning in 2019)

Technical Analysis

YSPSAH is currently a falling knife with high selling volume. Next support is at 2.33 followed by 2.23.

No comments:

Post a Comment