- Revenue increased by 5.8% while selling, marketing and administrative expenses merely increased by 1.9% (very good cost management).

- Gross profit margin is at 22.37% which is in line with the gross profit margin in the past years. (Average gross profit margin of Ahealth is between 21% - 25%).

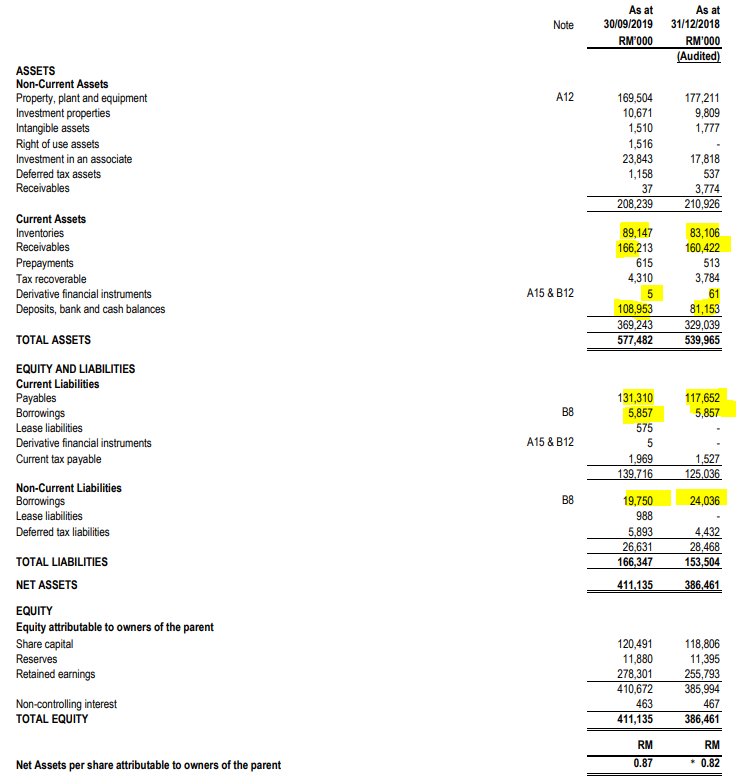

- Profit contribute from its associate (Straits Apex Sdn Bhd) increased 11% to 6 millions which contributes 12% to its profit before tax (In 2018, Straits Apex SB contributes 11% to Ahealth PBT).

- Cash at bank increased 34% to RM109 millions as compared to year 2018 (This proves Ahealth has very strong cash generating ability).

- Bank borrowings currently stood at RM25 millions (Ahealth generates RM50 million of operating cash flow in 9 months, meaning to say that Ahealth is able to settle its debts in no time)

- Revenue of Ahealth increased by 5.8% however its inventories increased by 7.2% (meaning the business is still is expected to grow in this range moving forward). Trade receivables increased by 3.6% (This is in line with the revenue growth) while trade payables increased by 11.6% (meaning to say Ahealth doesnt allow its debtors to own them money for too long while Ahealth have the ability to request for a longer credit term).

- Lets do a simple calculation: PBT for cumulative 9 months is RM47,850 + RM4,360(depreciation) + RM559(impairment) + RM960(inventories WO) - RM278 (forex loss) = RM54,007. So if we take away the additional one off expenses and the additional depreciation incurred by SPP Nova, Ahealth actually achieve RM 54 million of PBT which is even higher than previous year PBT of RM52 million.

- Strong cash flow from operating of RM50 million in 9 months as compared to RM34 million in 2018.

- As you can see that the amount that Ahealth spend on purchase of PPE reduced significant where it will further strengthen its cash flow.

- Ahealth achieves the highest quarterly revenue result of strong contributions from both private and public sector sale of Group branded pharmaceutical products.

- During the quarter, the Group’s wholly owned manufacturing subsidiary Xepa-Soul Pattinson (M) Sdn Bhd secured the EN ISO 13485:2016 accreditation for the Design and Development, Manufacture and Distribution of Sterile Eye Drops, a Medical Device category, certifying compliance with European Union standards.

- Ahealth also mentioned that they will record a lower sales in Q4 from its associates due to postponed orders.

Comments

- At current price of RM2.40, its PE is 20.3 which is the highest in Ahealth history. Average PE of Ahealth is 14.83 over the past 5 years. Assuming if Ahealth achieve an EPS of 11 sen for year 2019, At PE of 14.83, its share price is RM 1.63.

- Ahealth is a great company where its futures growth is visible. However 2019 is a resting year for Ahealth due to additional production cost by SPP Novo. Once the depreciation from SPP Novo is neutralized or mitigate by higher sales contributed by it, then its profit will started to grow again. Ahealth is worth to collect anything below RM1.80.

No comments:

Post a Comment